The accounts, which are set to become available on July 5, are for children born between 2025 and 2028

“Trump accounts,” the new investment vehicle for children that was part of the so-called One Big Beautiful Bill Act, could help parents create the next generation of millionaires — if they prioritize those savings for their kids’ retirements many decades from now.

The accounts will become available July 5, and American children born between Jan. 1, 2025, and Dec. 31, 2028, are eligible for a government-issued $1,000 contribution, according to Trumpaccounts.gov, the official website for the program. Parents or a child’s legal guardians will be the custodians of the account until the child turns 18, and contributions will be capped at $5,000 per year to start with.

More information is yet to be shared, such as how the funds can be invested and what financial institutions will manage these accounts, but strategies are already emerging for how to create long-term wealth for this generation of children.

“It is a gold rush for children for the future,” said Christopher Gandy, founder of the Legacy Wealth Group and president of National Association of Insurance and Financial Advisors.

Millions of American workers are unprepared for retirement and have little savings set aside for their old age. Workers in Generation X, who are the first to have to rely more heavily on their own preparations as opposed to company pensions, have a median $107,000 in household retirement accounts, according to a Transamerica Center for Retirement Studies report published in December.

The new accounts for children will mimic individual retirement accounts, although they come with a few very different rules, including lower contribution limits, no requirement for kids or their parents to use earned money to make contributions, and the ability for employers and private entities to also contribute.

One of the most powerful potential strategies for these accounts involves access to a Roth conversion when the child turns 18. The ability to invest from birth and then move the money to a Roth IRA, which allows savers to take tax-free withdrawals as well as avoid required minimum distributions later in life, could create the “largest block of millionaires we’ve ever seen in history, if done correctly,” Gandy said.

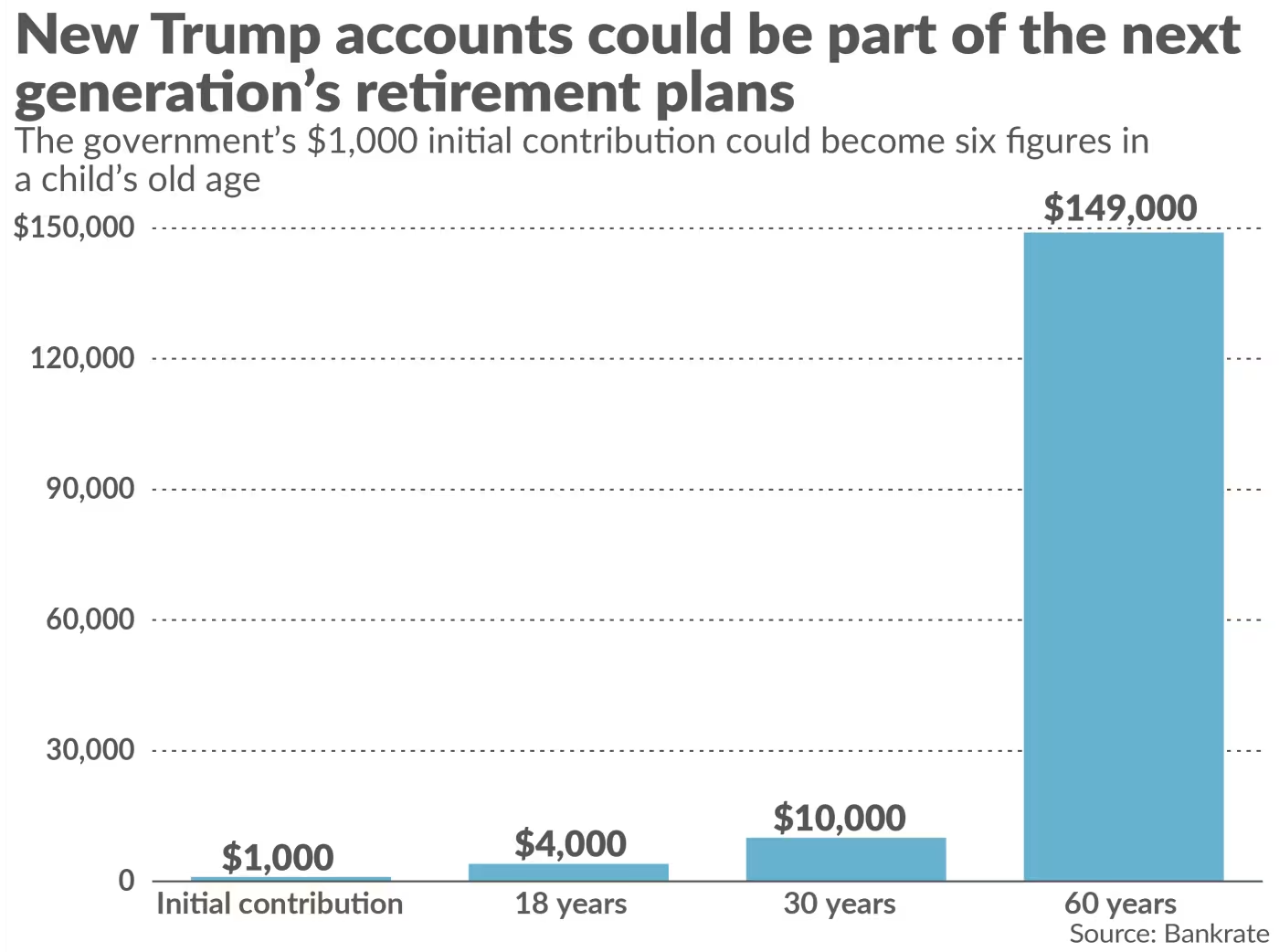

Take, for example, this Bankrate calculation: With just the $1,000 initial contribution from the government and assuming an inflation-adjusted return rate of 8%, a child’s account balance could be $4,000 in 18 years, $10,000 in 30 years and $149,000 in 65 years.

That calculation can be taken a couple of steps further, future-value calculators show. If the account received an additional $500 a year for 65 years, assuming the same return rate, the balance could grow to more than $1 million.

Not a replacement for other savings

Although these accounts could become part of the youngest generation’s retirement plans, they shouldn’t necessarily take priority over other savings vehicles for children, experts said.

For example, 529 plans are tax-advantaged investment accounts for education expenses, including tuition for college and graduate school, as well as kindergarten through 12th grade. Unused 529 funds can also be rolled into a Roth IRA, with restrictions such as a $35,000 lifetime limit.

“This is not a one-size-fits-all,” Stephen Kates, a financial analyst at Bankrate, said of the new accounts. “This is not going to take care of all of your goals or solutions. It is one avenue you can utilize.”

Before parents begin contributing to any accounts, whether it’s a Trump account, a 529 plan, a custodial account or a traditional savings account, they should think about what their goals are for the money, Kates said. “You can start to think of this in a waterfall fashion,” he said. “Where can my next dollar go and be best utilized?”

If the goal is saving for college, a 529 plan may work better than the other options, since annual contribution limits are significantly higher and distributions are tax-free when used for qualified education expenses. Someone hoping to amass enough for their child’s first down payment on a car or a home, meanwhile, might find custodial accounts attractive.

The new accounts add another layer to the investment strategies because they resemble a retirement account without the need for earned income, and they can be moved over to a Roth IRA, where they can grow tax-free for decades until the child retires. “A Roth conversion at age 18 would allow for decades of tax-free growth of what could be a substantial account balance,” according to Ed Slott and Company, a financial firm with a focus on IRAs. “That’s because up to $5,000 (indexed starting in 2028) of up to 18 years’ worth of contributions can be made to Trump Accounts by parents, grandparents or anyone else, even if the child has no earned compensation.”

The Internal Revenue Service has issued Notice 2025-68, which provides initial guidance on the new accounts. The notice states that the special rules that make these accounts different from traditional IRAs will end when the child turns 18, at which point typical traditional IRA rules would be in force, such as those for contributions, Roth conversions and taxation, including the 10% additional tax on early nonqualifying distributions.

More clarity on the new accounts is still needed, experts said. The government will have to publish precise rules and regulations in the coming year, including for what institutions will manage the accounts, whether account holders will pick their own investments or have preselected investments made for them, and what the logistics of contributions from various sources will be.

The information already available, however, seems promising for the youngest of children, whose savings “can grow and compound over a lifetime,” Gandy said. “This could be a potential for tax-free growth for young people we’ve never seen before.”